For most of the past two years, debate about stablecoins in payments has focused on the checkout screen: will consumers ever tap a wallet instead of a card?

Visa, Stripe, and Mastercard have answered with their capital. Visa now settles in USDC, Stripe bought Bridge, and Mastercard is acquiring BVNK.

Each move reflects the same read that stablecoins are becoming the settlement and liquidity layer beneath existing brands, and whoever controls that layer controls the economics of the next payment cycle.

Chainalysis put adjusted stablecoin volume at $28 trillion in 2025 and projected it could reach $719 trillion by 2035 on organic growth, with a more aggressive scenario approaching $1.5 quadrillion.

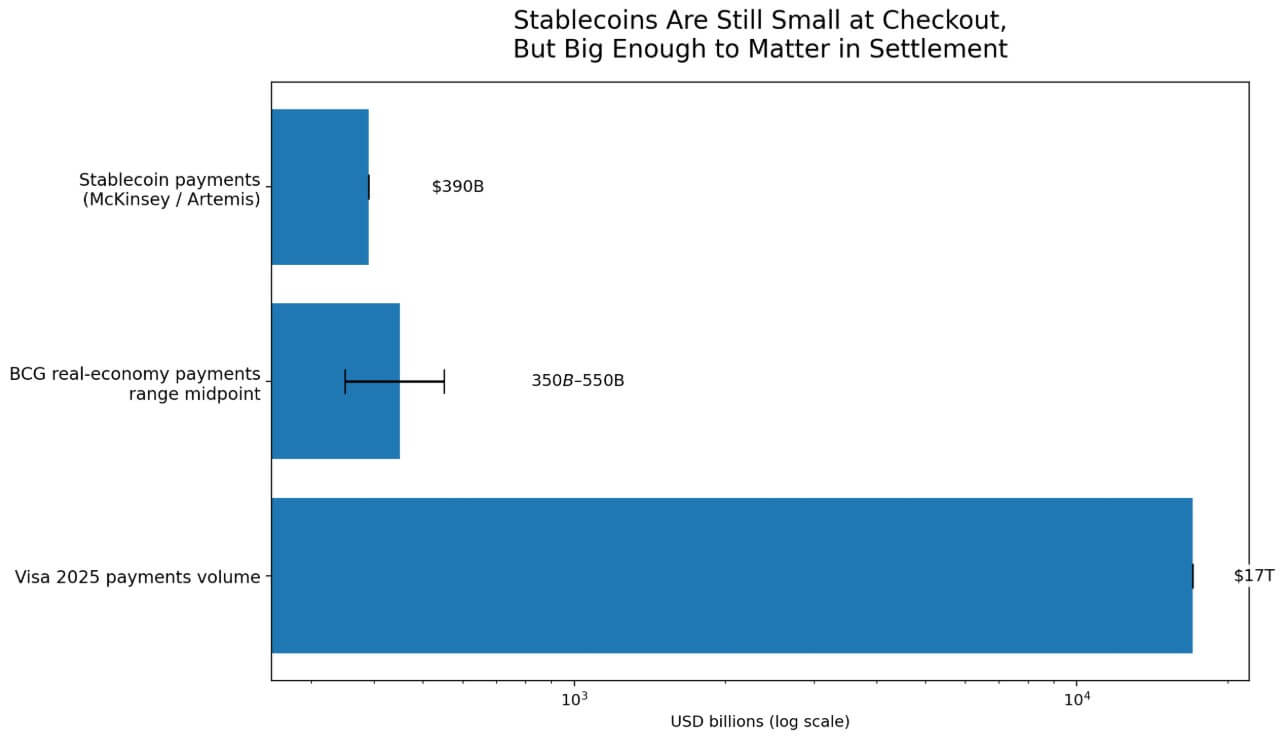

The grounding comes from McKinsey and Artemis, which estimate actual stablecoin payments at about $390 billion annually, a figure corroborated by BCG's $350-$550 billion range, excluding non-economic and trading flows.

At those levels, stablecoins represent roughly 2.3% of Visa's $17 trillion in payments volume in 2025.

Stablecoins can reprice settlement economics at 2.3% penetration because settlement and checkout operate on separate infrastructure.

A logarithmic bar chart shows stablecoin payments estimated at $390 billion by McKinsey/Artemis and $350–$550 billion by BCG, compared with Visa's $17 trillion in 2025 payment volume.

A logarithmic bar chart shows stablecoin payments estimated at $390 billion by McKinsey/Artemis and $350–$550 billion by BCG, compared with Visa's $17 trillion in 2025 payment volume.Many hybrid stablecoin payment flows never appear as on-chain merchant transactions. Crypto card transactions typically execute on traditional card rails, while the blockchain captures only issuer inflows and outflows.

A stablecoin settlement layer can expand commercially without ever becoming visible at the point of sale.

Three bets on the same stack

Visa launched USDC settlement in the US in December 2025. By Mar. 25, its global stablecoin settlement activity had reached an annualized run rate of $4.6 billion across more than 130 stablecoin-linked card programs in more than 50 countries.

Visa's own framing centered on treasury modernization and settlement efficiency, as its Canton Network effort extended that logic into payment, settlement, and treasury use cases for banks, a deliberate push to own the orchestration layer for institutional stablecoin flows.

By March 2026, Bridge-enabled stablecoin-linked cards had gone live in 18 countries, with plans to reach 100-plus by year-end, and Visa was evaluating settlement optionality, faster fund movement, and simplified blockchain abstraction for institutions.

Stripe's 2025 annual letter, published Feb. 24, reported stablecoin payments volume doubled to around $400 billion, with an estimated 60% in B2B flows, while Bridge volume more than quadrupled.

Bridge had won conditional OCC approval for a national trust bank covering custody, issuance, orchestration, and reserve management.

Mastercard's March 2026 agreement to acquire BVNK for up to $1.8 billion came alongside a statement that digital currency payment use cases had already reached at least $350 billion in 2025, with the incremental opportunity in cross-border remittances, payouts, peer-to-peer transfers, and B2B payments.

Mastercard also cited speed and programmability as answers to treasury management and commercial flow pain points.

Three companies, three products, and M&A strategies, one shared thesis: stablecoin settlement is embedding itself into payment infrastructure before any consumer-visible checkout revolution arrives.

| Visa | USDC settlement in the U.S.; 130+ stablecoin-linked card programs across 50+ countries; Canton Network push | Stablecoins are being treated as a settlement and treasury modernization layer, not just a checkout experiment | Merchant settlement, treasury operations, card-issuing orchestration, institutional settlement | Settlement + orchestration layer |

| Stripe / Bridge | Stripe acquired Bridge; stablecoin volume around $400B in 2025; estimated 60% B2B; trust-bank path for custody, issuance, orchestration, and reserves | Stripe is building enterprise-grade stablecoin infrastructure for business flows, not retail-only crypto payments | B2B payments, developer APIs, custody, issuance, reserve management, enterprise infrastructure | Developer/compliance stack |

| Mastercard / BVNK | Mastercard agreed to acquire BVNK; digital-currency payment use cases at $350B+ in 2025 | Mastercard sees stablecoins as a way to upgrade cross-border and commercial money movement while keeping fiat connectivity | Cross-border remittances, payouts, P2P, B2B payments, treasury/commercial flows | Corridor distribution + commercial flows |

The Federal Reserve confirmed in an Apr. 8 note that stablecoin market capitalization reached $317 billion as of Apr. 6, up more than 50% since early 2025.

Congress enacted the GENIUS Act in July 2025, supplying the formal US legal framework that institutional adoption requires.

Citi's September 2025 base case put stablecoin issuance at $1.9 trillion by 2030, supporting roughly $100 trillion in annual transaction activity, and projected more than $1 trillion in incremental demand for US Treasuries at that scale.

At $317 billion in current capitalization, the stablecoin market is about 16.7% of Citi's 2030 target, which is far enough along that the largest payment networks have committed capital, yet early enough that the outcome stays open.

What to expect

The bull case turns on how fast compliance infrastructure can absorb stablecoin settlement at enterprise scale.

Regulatory clarity arrived through the GENIUS Act, with Visa and Bridge targeting 100-plus countries by year-end. Stripe and Bridge are building toward regulated custody and reserve management.

If enterprises can treat stablecoin settlement as routine treasury operations, cross-border payouts, merchant settlements, and B2B flows will migrate to on-chain rails faster than any single forecast can capture.

In that setting, Citi's $1.9 trillion issuance projection becomes a floor, and the firms that own orchestration, compliance, reserves, and interoperability standards capture the structural economics of the new stack.

The bear case requires open stablecoin rails to remain fragmented long enough for incumbents to absorb the functionality as a proprietary feature.

The Fed's April 2026 note flagged more complex intermediation chains, vertical integration, opacity, and run risk as vulnerabilities that push regulated institutions toward permissioned alternatives.

Citi's own analysis suggests that bank-issued tokenized money could exceed open stablecoins in institutional volume, with adoption anchored in corporate treasuries and capital markets, where compliance requirements favor closed networks.

In that outcome, stablecoins continue to expand, while the economic benefits accrue to regulated, permissioned systems. Incumbents deploy stablecoins as a feature, and the plumbing stays proprietary.

| Bull case | Stablecoin settlement becomes routine for treasury, cross-border payouts, merchant settlement, and B2B flows | Visa, Stripe/Bridge, Mastercard, and compliant infrastructure providers | Stablecoins become a default back-end rail beneath existing payment brands |

| Base case | Stablecoins expand steadily in selected corridors and enterprise workflows, but checkout remains mostly unchanged | Incumbents plus a handful of infrastructure specialists | A hybrid system emerges: cards and banks on the front end, stablecoins increasingly underneath |

| Bear case | Open stablecoin rails stay fragmented; incumbents absorb stablecoin functionality as a proprietary feature | Regulated incumbents and permissioned-network operators | Stablecoins still grow, but mostly inside closed or semi-closed systems |

| Control-point battle | Orchestration, compliance, reserves, FX management, and interoperability standards become decisive | Whoever owns the back-end stack rather than the checkout screen | The key question shifts from who owns the card to who owns money movement |

The control points

Visa, Stripe, and Mastercard are each running for different segments of the back-end stack: Visa through settlement and card-issuing orchestration, Stripe and Bridge through developer APIs, B2B infrastructure, and regulated custody, and Mastercard through cross-border corridors, remittances, and commercial treasury.

Their positioning reflects a shared read that the decisive contest runs through orchestration, compliance, reserves, foreign exchange management, and interoperability standards.

Chainalysis projects stablecoin transaction volumes could intersect Visa and Mastercard off-chain volumes between 2031 and 2039. The more consequential inflection preceded that projection by years.

The largest card networks began redesigning their settlement and payout infrastructure around stablecoins even as stablecoins accounted for less than 3% of global payment flows.

The firms that build the most defensible positions in orchestration and compliance over the next 36 months will determine who captures the economics of that intersection.