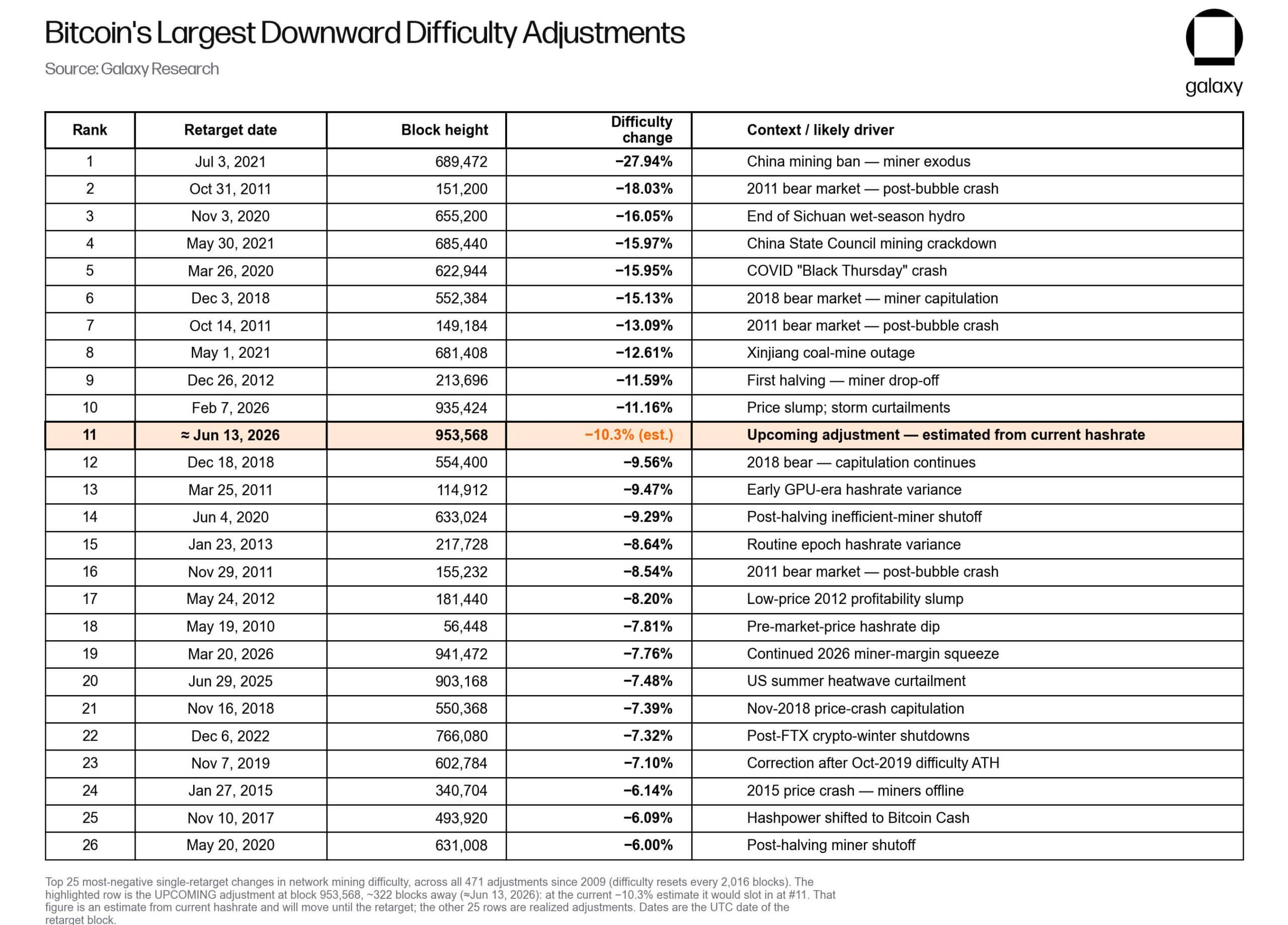

The Bitcoin network is poised to execute one of the largest downward adjustments to its mining difficulty in its 17-year history this weekend, a stark reflection of the severe margin compression forcing operators to take hardware offline.

The automated recalibration, scheduled to occur on June 13 at block height 953,568, is projected to slash the network’s difficulty by approximately 10.3%. This shift will drop the target metric from 138.96 trillion to roughly 124.25 trillion.

This would also be the second-largest drop this year, behind an 11.16% decline in February.

Additionally, the decline will mark the 11th-largest negative difficulty adjustment since the inception of the digital asset in 2009, signaling a significant retreat in the aggregate computational power securing the blockchain.

A year of compounding financial strain

The impending reduction highlights a remarkably brutal calendar year for digital asset infrastructure providers, characterized by collapsing revenue and shrinking network demand.

With this upcoming adjustment, the current year will account for three of the top 20 downward difficulty drops in Bitcoin history, placing it on par with the most volatile periods in the network's life cycle.

This rapid decompression is evident in the absolute scale of the network's retrenchment. Mining difficulty has reduced from near 150 trillion at the beginning of this year to the upcoming projected 126 trillion level, representing a 16% decline year-to-date.

Historically, only three calendar years have ever recorded three or more top-20 difficulty drops. The record is held by 2011, which saw four such appearances during an era of extreme early-stage asset volatility.

Bitcoin Mining Difficulty (Source: Galaxy Digital)

Bitcoin Mining Difficulty (Source: Galaxy Digital)With the current year only hitting its midpoint, infrastructure analysts warn that further large-scale downward adjustments remain a distinct possibility if market conditions fail to materialize a meaningful recovery.

The primary catalyst for this systemic retrenchment is the relentless downward pressure on the asset's underlying spot price.

Data from CryptoSlate shows that Bitcoin has declined nearly 30% year-to-date, a macro downtrend capped most recently by a steep 15% drop in June that dragged the asset into a tight trading range of $62,000 to $63,000.

For mining operations running on narrow profit margins, particularly those employing older hardware configurations or navigating high-cost power purchasing agreements, this compounding price erosion has flipped businesses from marginally profitable to structurally unsustainable almost overnight.

BTC miners are operating at the breakeven threshold

These severe price struggles have brought the entire sector to a critical juncture where the average operator is fighting just to stay in the black.

Data compiled by Capriole Investments, a quantitative digital asset fund, indicates that Bitcoin is currently trading in line with its average aggregate production cost, which is approximately $62,650.

Bitcoin Production Cost (Source: Capriole)

Bitcoin Production Cost (Source: Capriole)In an X post, Charles Edwards, founder of Capriole Investments, noted:

“Miners are now just breaking even on average.”

Edwards pointed out that historical long-term value windows for the asset typically materialize when the market price hovers between the total production cost and the bare electrical cost, the latter of which currently stands near $50,000.

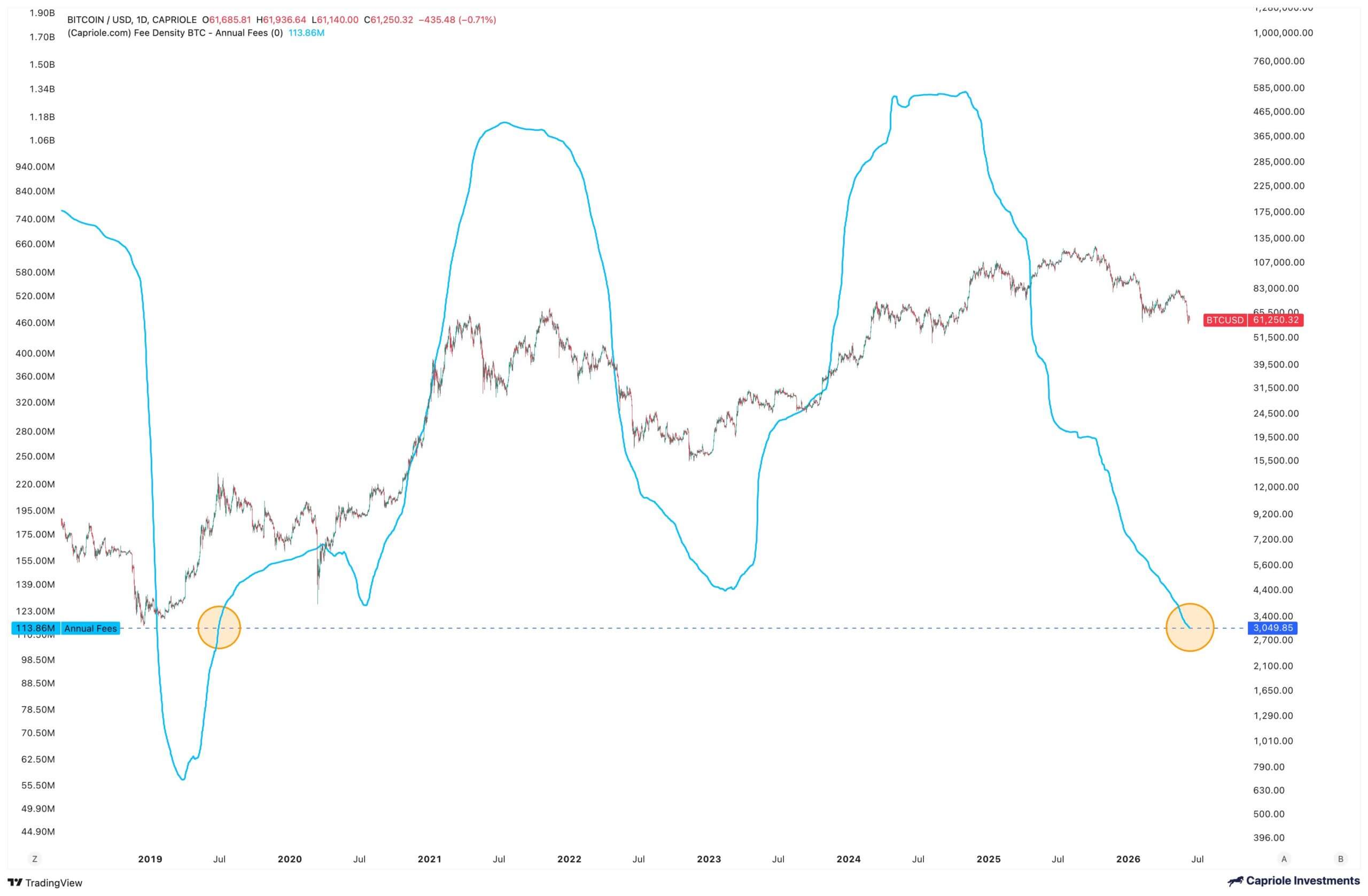

Compounding the pressure of a lower spot price is a substantial contraction in organic network fees.

The annual transaction fees earned by miners, excluding the fixed software-issued block rewards, have dropped over a trailing 12-month period to levels not seen since 2019.

This multi-year low in transaction-throughput revenue, following successive block reward halving events, has driven a broader structural shift within the publicly traded digital asset infrastructure sector.

Bitcoin Mining Fees (Source: Capriole)

Bitcoin Mining Fees (Source: Capriole)With transaction fee revenue under pressure and global demand for high-performance computing (HPC) in artificial intelligence expanding, multiple public mining firms are actively diversifying their data center capacities away from pure-play cryptocurrency mining and toward AI compute hosting.

Cheap rigs and efficiency plays mask miner pain

Despite the clear operational headwinds, the absolute network hashrate has remained deceptively resilient.

Industry data suggests this durability is driven by a stark divergence in hardware efficiency, as capitalized operators aggressively replace legacy machinery with next-generation units.

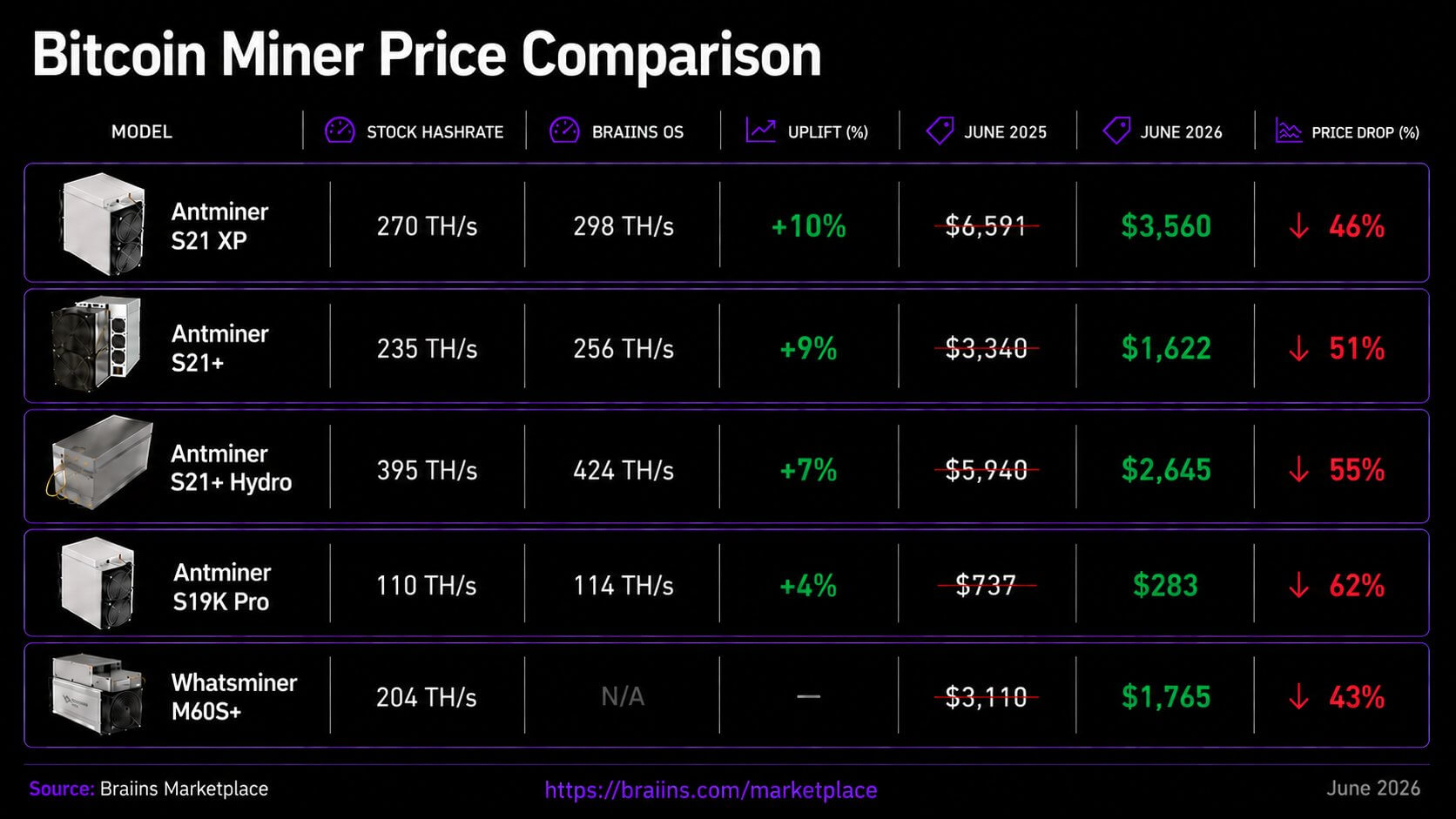

According to data from the Bitcoin mining platform Braiins, secondary-market prices for mining hardware have plunged by as much as 62% over the past year, reducing the capital expenditure required for premium fleet upgrades.

The efficiency gap between legacy and modern hardware explains why total network computational power has not fallen as dramatically as spot prices.

For instance, an older-generation Antminer S19j Pro generates 104 terahashes per second (TH/s) while consuming 3,068 watts on stock firmware, resulting in an efficiency rating of 29.5 joules per terahash (J/TH). In contrast, the newer Antminer S21 XP delivers 270 TH/s at 3,645 watts, achieving an efficiency of 13.5 J/TH.

Bitcoin Miner Price Comparison (Source: Braiins)

Bitcoin Miner Price Comparison (Source: Braiins)When optimized with custom firmware, the newer unit can reach 298 TH/s at the same power draw, dropping its efficiency rating to 12.2 J/TH.

This represents a 59% reduction in energy consumption per terahash compared to the older model.

Consequently, well-capitalized enterprises are exploiting low-cost hardware markets to phase out obsolete rigs, keeping aggregate network hashrate elevated even as less efficient operations close.

Stress builds, but capitulation remains incomplete

While these efficiency upgrades have allowed well-capitalized firms to stay afloat, broader on-chain data suggests the industry at large remains under stress.

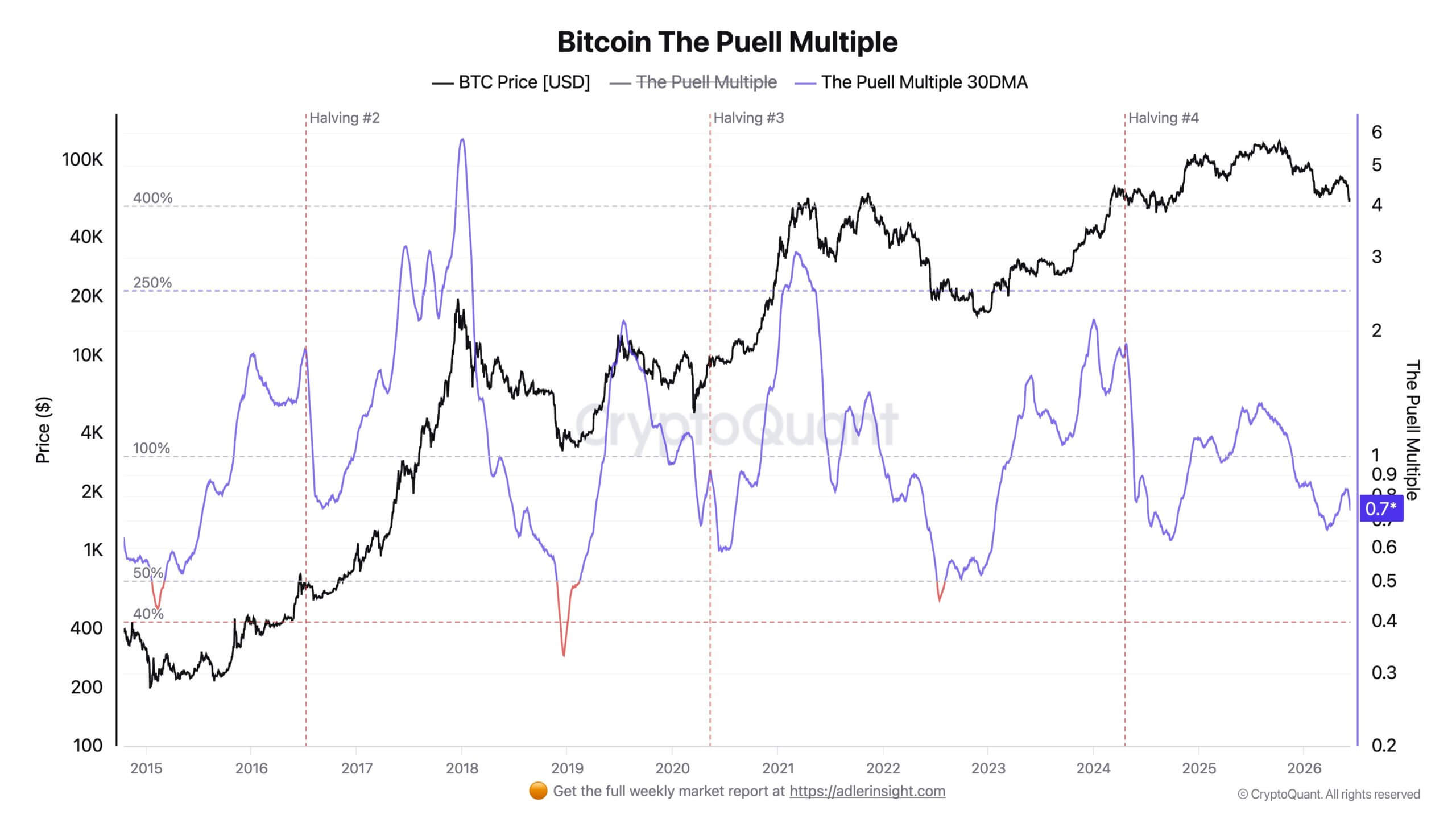

CryptoQuant analyst Axel Adler said several miner indicators have moved into stress levels similar to those seen after past halvings, though they have not yet reached the capitulation phases that marked the 2018 and 2022 market bottoms.

One of those gauges, the Puell Multiple, compares miners’ daily revenue with its one-year average. The indicator has been trending lower and stood near 0.74 on June 10, while the raw reading fell to 0.58.

Bitcoin Puell Multiple (Source: CryptoQuant)

Bitcoin Puell Multiple (Source: CryptoQuant)Readings below 1 typically show that miner revenue is running below its annual average. Lower readings point to deeper financial pressure across the sector.

Adler said the current level is close to where the metric traded around the 2024 halving, when Bitcoin moved between roughly $55,000 and $68,000. Previous cycle lows were much more severe. The 30-day average fell to 0.45 near the 2022 market bottom and dropped to 0.33 in December 2018.

The difference is important for the current setup. Miner revenue is weakening, but the industry has not yet seen the broad shutdowns that usually define full capitulation.

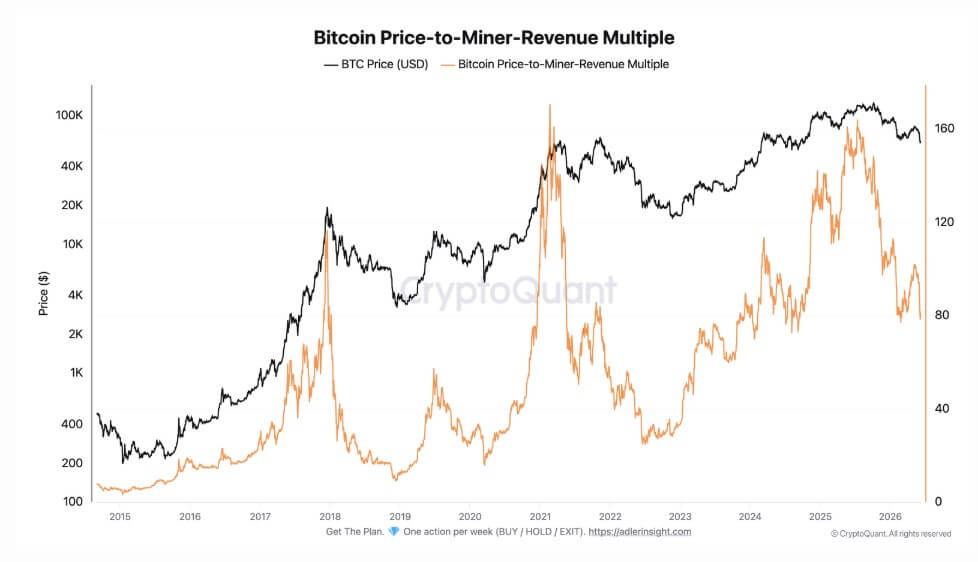

Another metric, the price-to-miner-revenue multiple, also points to a cooler market. The gauge compares Bitcoin’s price with miners’ rolling annual revenue per coin. It recently stood near 80, down from peaks of about 160 in July 2025 and February 2021.

Bitcoin Price to Miner Revenue (Source: CryptoQuant)

Bitcoin Price to Miner Revenue (Source: CryptoQuant)At the 2022 bottom, the metric fell to 33. That suggests the market premium over miner revenue has narrowed but has not disappeared. A deeper capitulation signal would likely require a move toward the 40 to 50 range or a longer stretch of depressed miner income.

A separate miner capitulation gauge, which tracks Bitcoin’s price change since the last difficulty bottom, has also moved into a pressure zone. It recently showed a drawdown of about 21%, compared with roughly 8% at the start of June.

The move shows that Bitcoin’s price has continued to fall even after the network adjusted its mining difficulty downward.

The indicator has crossed the 15% threshold that analysts often associate with heightened miner stress. In 2022, the worst reading reached roughly 39%.

A further decline in Bitcoin, without a recovery in price or mining difficulty, could deepen the stress signal and raise the risk of forced selling or additional miner shutdowns.

Bitcoin mining's next test comes after the reset

The sector's true durability will be tested immediately after the upcoming June 13 difficulty reduction.

The recalibration should provide some much-needed relief for the miners that manage to remain online, as lower difficulty means each unit of active hashrate has a better chance of earning block rewards.

In past cycles, difficulty drops have sometimes helped stabilize mining conditions, marking periods when weaker operators had already absorbed the worst of the pressure.

The challenge this time is that the relief arrives while several revenue lines remain historically weak.

As established, Bitcoin’s price is trading directly at production-cost estimates, hashprice is near breakeven for many firms, and fee revenue has fallen to multi-year lows. The halving has also reduced the baseline subsidy that miners rely on during periods of low transaction activity.

For traders, miner stress has historically been watched as a signal that Bitcoin may be approaching better long-term value zones.

When miners are forced to sell, shut down, or upgrade, the market often moves through one of the more painful parts of the cycle. But the current data suggests pressure is still developing rather than fully exhausted.

The next few weeks will show whether the difficulty cut is enough to slow the strain. A recovery in Bitcoin’s price above the production-cost zone, a rebound in transaction fees, or a stabilization in the Puell Multiple would suggest miner pressure is easing.

Conversely, another leg lower in Bitcoin would put the sector under a more severe test. If price weakness deepens while hashprice remains depressed, more older machines could be switched off, and miner reserves could come under renewed scrutiny.